FinTech: Transparency, Decentralisation & Blockchain

The 2008 financial crisis was a blessing in disguise (a very very good disguise) for FinTech; banks had to deal with the new fines, blocks & regulations imposed by governments to “punish” those responsible and ensure that the same mistakes were not repeated.

A whole new school of thinking was necessary to surpass the crisis – Hence Blockchain.

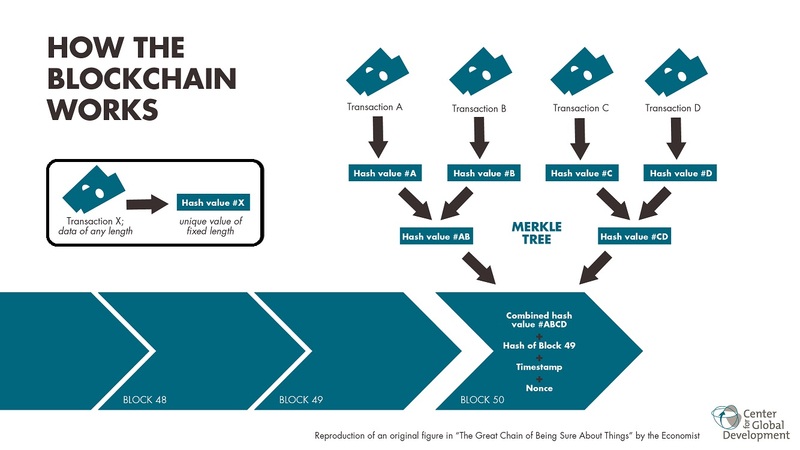

The Blockchain system is a distributed or “Shared ledger” that multiple parties are using which allows parties to collaborate without having to trust each other. Each process or “block” must be authenticated and validated by over 50% of the other parties or “miners” before it is accepted and added to the Blockchain. In essence every process is audited making it more transparent, fast and cheap than traditional methods.

These two new innovations lead to the Digitisation of banks - Making mortgages & loans more transparent via the Blockchain system i.e. customer can see and access the entire supply chain and order of transaction behind their loans, mortgages & investments.

Henri Arslaian, the FinTech Revolutionist, believes that this is only the beginning.

According to Citi Bank 30% of banking jobs will disappear by 2020 due to Digitisation. Intermediaries such as Correspondent Banks & Governments that perform “business logics” (currency exchange, inflation, International money transfers etc.) are becoming obsolete as they are costly, slow and exclude a large amount of the population (2-2.5 bill. people have no access to a physical bank).

However, decentralised systems are not user friendly and they require a centralised service or platform e.g. the internet needs Google & Hotmail. Similarly, “Blockchain is going to be the infrastructure in the background” and centralised services will be built on top of it. - Henri Arslaian